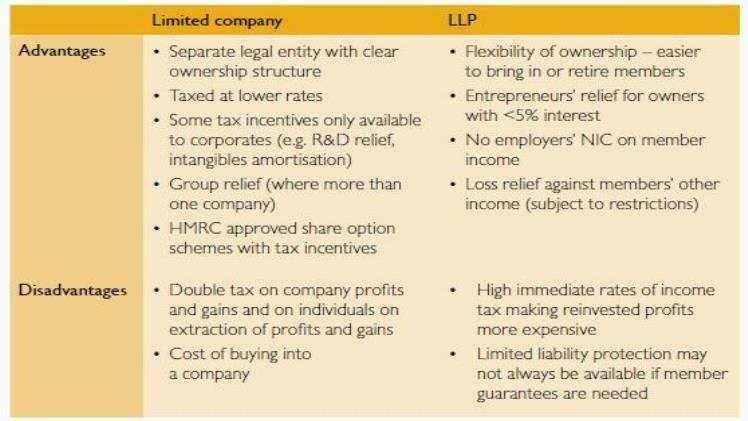

There are many reasons entrepreneurs choose to opt for a Private Liability Partnership (LLP) registration instead of a private limited Company incorporation. They are easier to establish and are relatively easy to manage in daily routines. Also, they have less risk of being a compliance issue if there’s very little work. Many entrepreneurs find it beneficial to start their business by establishing an LLP in this way. This article will examine the many advantages and disadvantages associated with an LLP for India. To know more click Dinar

Advantages of an LLP

There are a few advantages to incorporating an LLP in India:

There is no minimum contribution.

The minimum capital requirement for an LLP. An LLP can be created with the lowest amount of capital. Additionally, the contribution of a partner could comprise tangible, immovable or movable or intangible property or any other advantages to the LLP.

No limitation on the proprietors of businesses

An LLP needs a minimum of two partners, and there is no limitation on the number of members. It is different from a private limited company, where there is a limit that it cannot have more than 200 members.

Lower cost of registration

The cost to register an LLP is relatively low compared to the expense of incorporating a private limited company or a public-owned limited business. But, the distinction in the price of the registration of an LLP in comparison to a Private Limited Company has come down over the last few days.

There is no requirement for a compulsory Audit.

Regardless of their share capital, a public or private company must have the accounting audited. However, in the cases of LLP, the law does not provide for any such mandatory requirement. It is thought of as a significant compliance advantage. It is believed that a Limited Liability Partnership is required to have the tax audit completed only if it:

- The contribution of the LLP exceeds the amount of Rs. 25 Lakhs or

- The turnover per year of the LLP is more than the amount of Rs. 40 Lakhs

Taxation Aspects on LLP

To be tax-efficient, LLP is treated equally with partnership companies. Therefore, LLP is responsible for the taxation on income and part of its partners’ shares as LLP is not taxable. It means that no dividend tax is due. The income tax code’s ‘deemed dividend’ provision does not apply to LLP. Section 40(b) (b): Interest payable for partners, all payments of bonus, salary commission, or remuneration that is deducted as a deduction.

Dividend Distribution Tax (DDT) is not applicable.

Suppose corporation owners decide to take profits from the business. In that case, the company will be liable for additional tax liabilities as DDT at 15 per cent (plus surcharge and the education tax) is owed to the company. But, no such tax is due in the case of an LLP, and the owners can quickly take the earnings of an LLP.

Disadvantages of and LLP

An LLP also comes with a variety of disadvantages when compared with a private limited company, such as:

Penalties for Non-Compliance

Even if an LLP is not involved in any activities, it is required to submit its income tax return and an MCA annual return every year. If an LLP does not offer its Form 8 or Form 11 ( LLP Annual Filing), the fee assessed of Rs.100 per day will be considered. There is no maximum penalty; it could reach thousands of dollars if the LLP still needs to complete its annual return in several years.

If you are a sole partnership or sole proprietorship, you are not required to file an annual tax return. Therefore there are no penalties in the Income Tax Act that would be applicable.

Inability to Have Equity Investment

An LLP doesn’t have the notion of shareholding or equity-like an enterprise. Thus, angel investors’ Venture capital, HNIs, and private equity funds cannot be part of an LLP in the form of shareholders. So, most LLPs will have to depend on promoters’ funding and financing from debt.

Higher Tax Rate on Income

The income tax for a business with a turnover of less than Rs.250 million is 25%. (Further cut in 2019 for companies that are new and that are involved in producing). LLPs are taxed at 30%, regardless of their turnover.